Source: Preliminary Steps Toward a Universal Economic Dynamics for Monetary and Fiscal Policy | NECSI

Cite as:

Yaneer Bar-Yam, Jean Langlois-Meurinne, Mari Kawakatsu, Rodolfo Garcia, Preliminary steps toward a universal economic dynamics for monetary and fiscal policy, arXiv:1710.06285 (October 10, 2017).

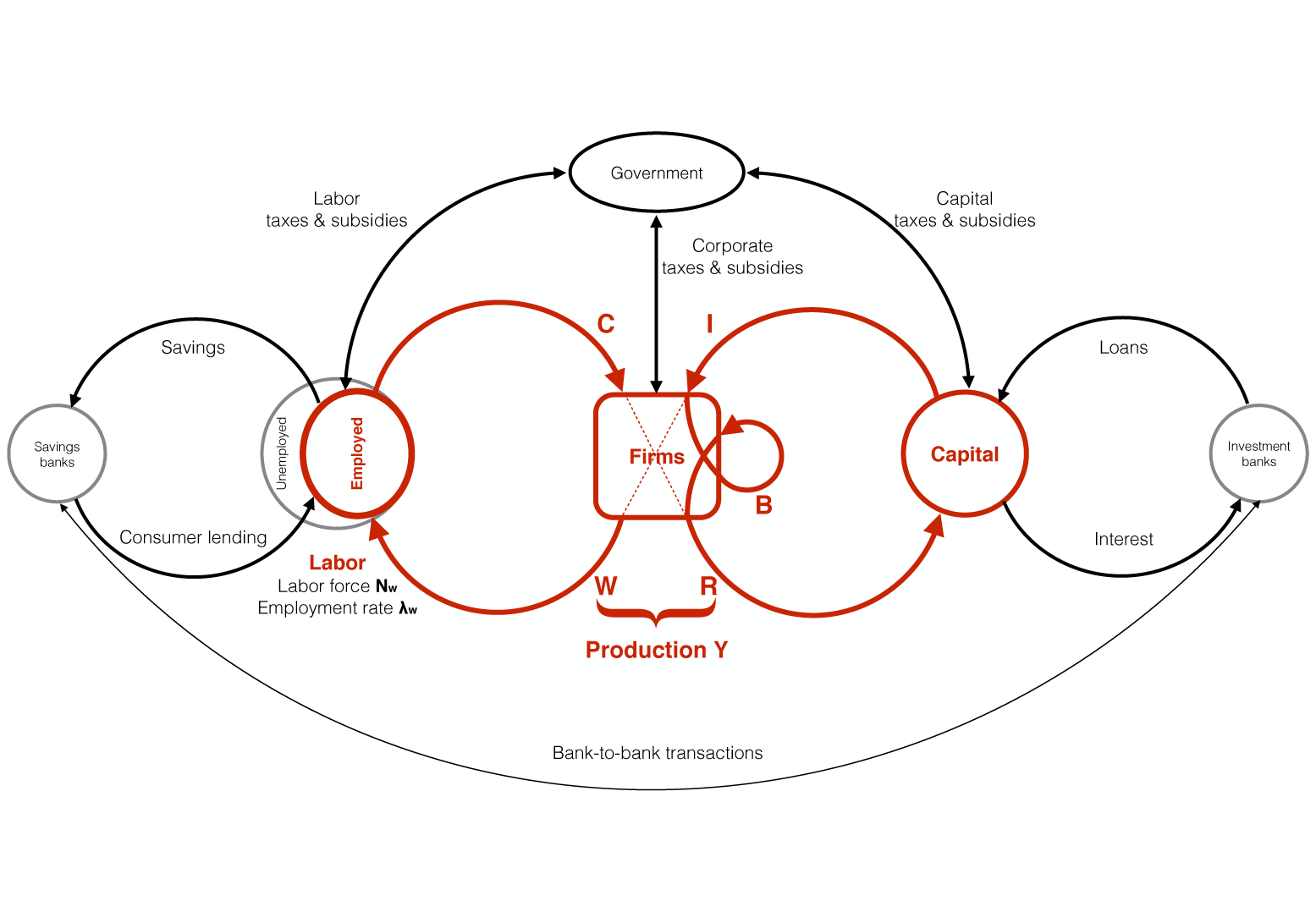

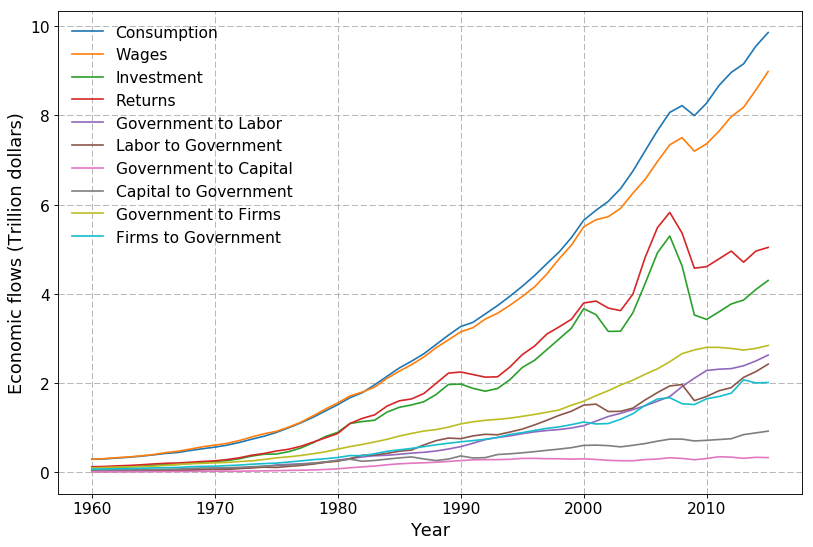

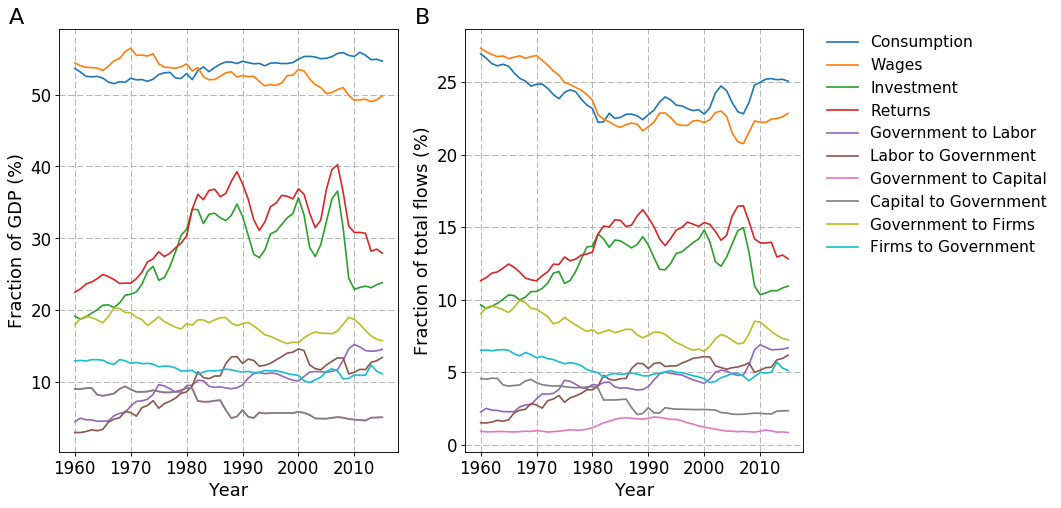

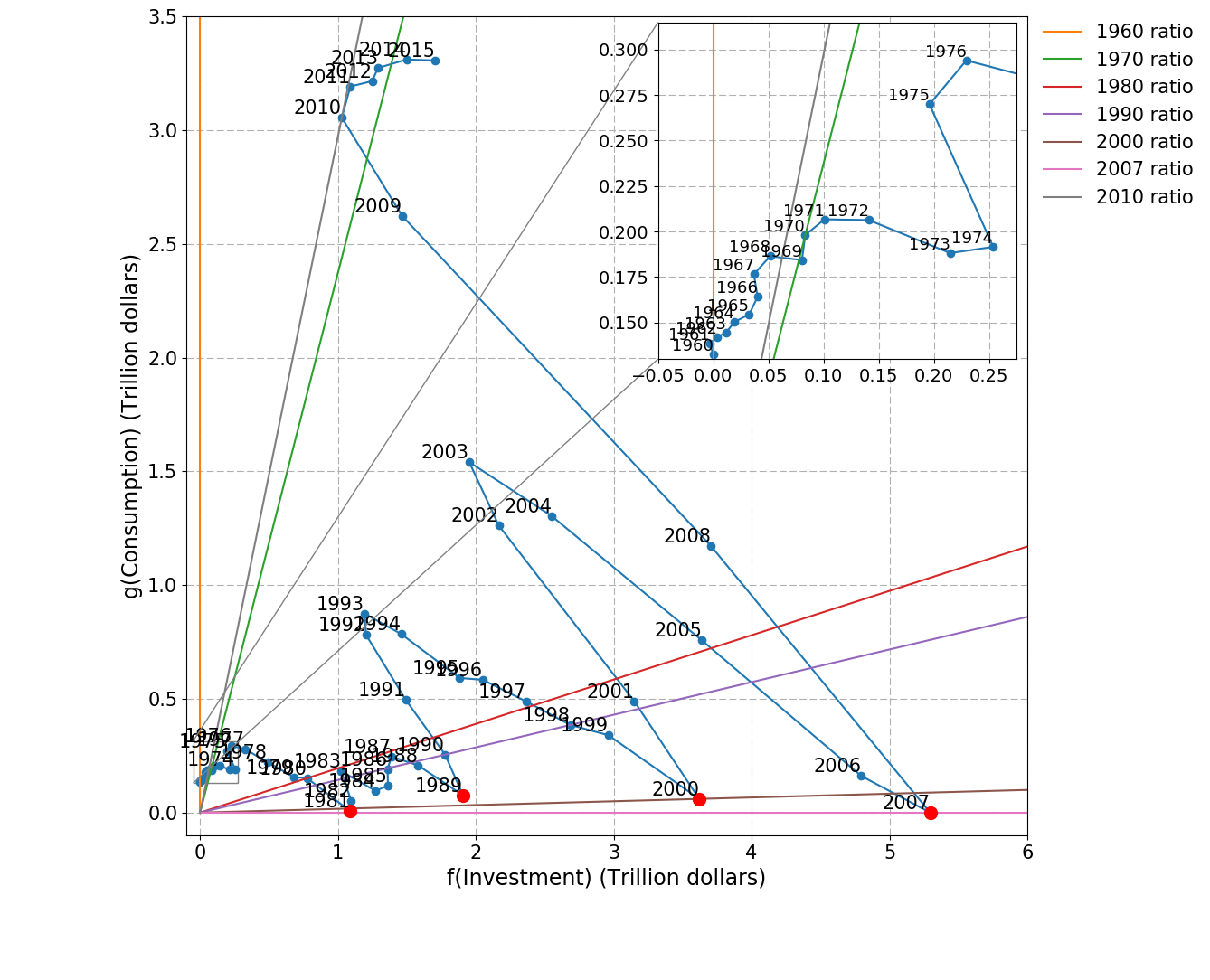

We find that the current approach, which considers the overall supply of money to the economy, is insufficient to effectively regulate economic growth. While it can achieve some degree of control, optimizing growth also requires a fiscal policy balancing monetary injection between two dominant loop flows, the consumption and wages loop, and investment and returns loop. … We further show that empirical evidence is consistent with a transition in 1980 between two regimes—from an oversupply to the consumption and wages loop, to an oversupply of the investment and returns loop. … Our analysis supports advocates of greater income and / or government support for the poor who use a larger fraction of income for consumption. This promotes investment due to the growth in expenditures. Otherwise, investment has limited opportunities to gain returns above inflation so capital remains uninvested, and does not contribute to the growth of economic activity.

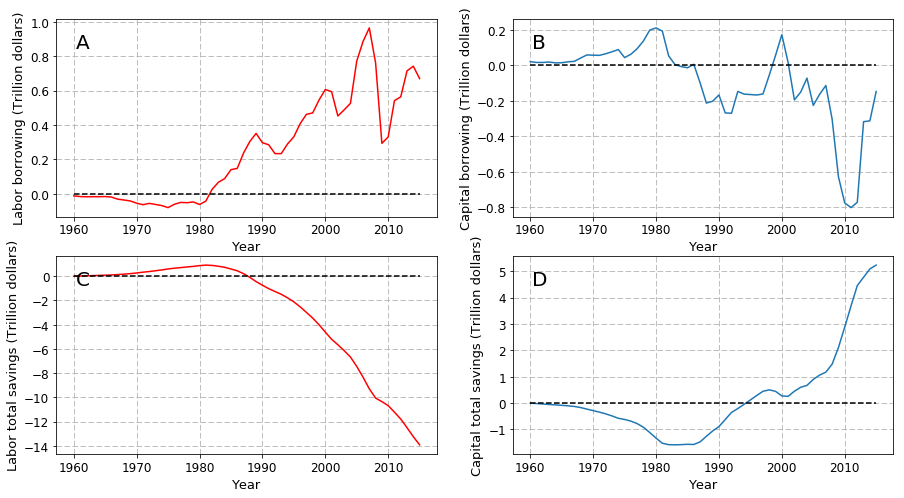

Since 1980 consumers have accumulated trillions of dollars of debt, and the wealthy have accumulated trillions of dollars of savings that is not invested because there is nothing to invest in that will give returns. … No matter how much money investors have, these so-called “job creators” do not create jobs when consumers don’t have money to buy products. Increased economic activity requires both investment and purchase power to pay for the things the investment will produce. … Reaganomics moved things too far toward the wealthy, so shifting the flow in the other direction has to be done in the right measure.